Our partners at yCharts wrote an excellent blog talking about the effects of the Federal Reserve's Rate Hikes or Pauses, using historical and correlative data to educate individuals on what different financial vehicles may do, or at least have done when the Fed moves their key rates. Here is a synopsis, but be sure to view the full bit over on their website HERE and be sure to look at their article for all of the charts that explain each category!

What Happens After A Fed Rate Hike?(Or Pause?)

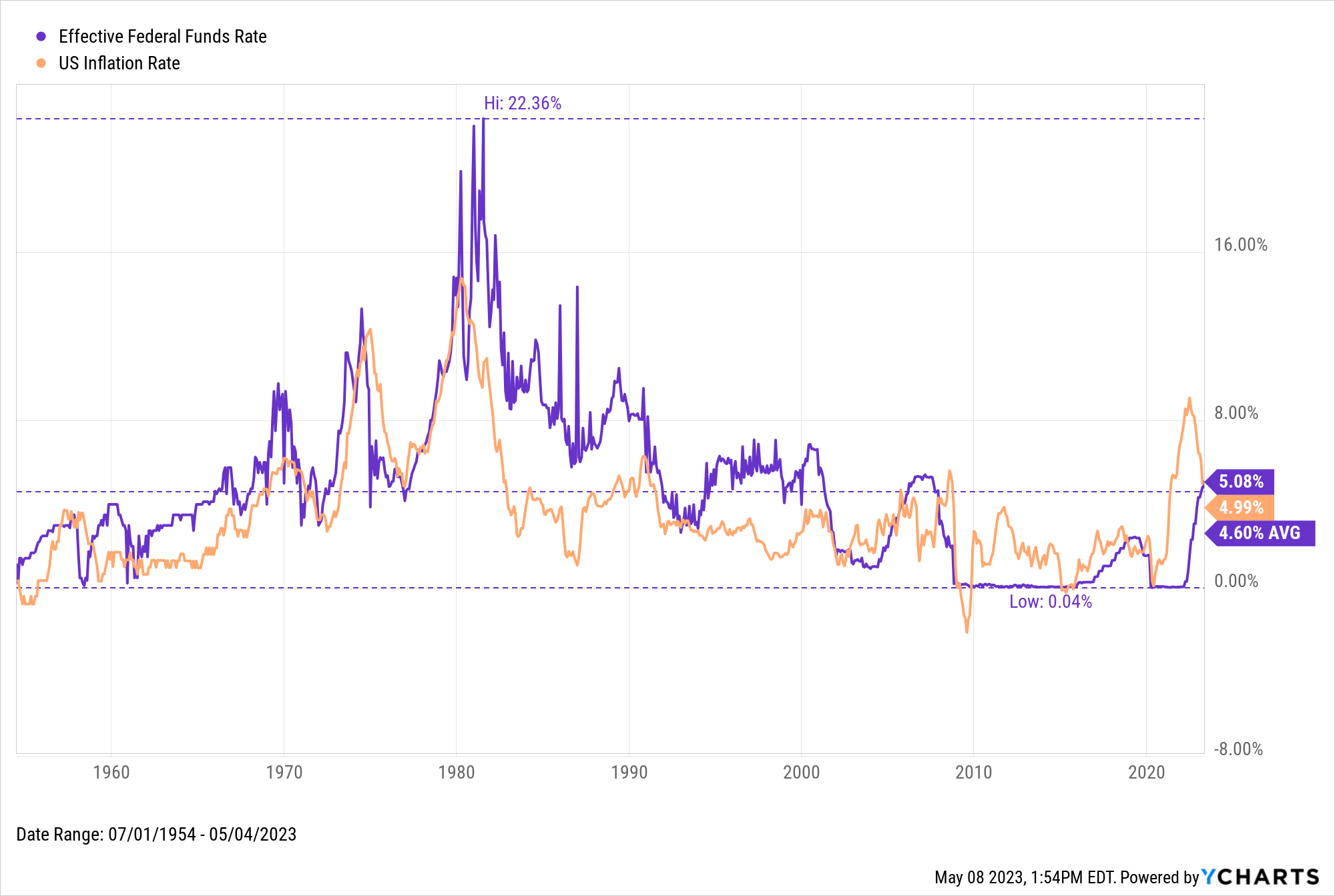

At the beginning May, the US Federal Reserve hiked rates for the 10th consecutive time to a range of 5-5.25%. Since the Fed's hawkish period began in March of 2022, we've seen inflation drop about 40% from the high falling from 9.1% down to 4.99% annualized pace. In 2022 the S&P 500 index ended the year down over 18% but has now rebounded 7.5% through the first quarter of 2023, even with inflatino remaining above the Fed's long term target of 2%. Because of these unprecedent rates hikes, we've seen other cracks emerge in the economy including three major banks failures and a major pause in capital expenditures from coprorations as they look to whether the likely economic slowdown.

With everyone guessing what the Feds next steps may be, gaining hints from Fed officials removing phrases like 'additional policy tightening may be appropriate' from statements, perhaps investors can finally unfasten their seatbelts as rates might be at their cruising altitude.

For some, the Federal reserve rate seems like something that doesn't effect their day to day operations...but let's take a look into how powerful their decisions are and the chain reactions that moving the prime rate causes.

How Bonds Are Affected by Fed Rate Hikes

Short term treasury rates are most direction affected by the Fed's monetary policies, as stated by the Fed itself; historically moving lock and step with the target fed funds rate. Oppositely, long term rates typically don't follow the rate as closely even though in generally they move in the same direction.

The key for investors, however, is that bond market values typically decline as rates go up. In a rising rate environment, new bonds offering higher interest payments will be issued, causing existing ones to decline in price. If rate hikes were to pause, the prices of existing bonds could stabilize or even regain value, as their yields become increasingly competitive in comparison to newer offerings.

This fact caused the 60/40 portfolios to experience their worst performance in nearly 40 years during 2022.

How Consumers Are Affected by Fed Rate Hikes

Prime Loan Rate

The Prime Loan Rate is the rate at which banks lend to their most creditworthy clients, and it is strongly correlated with the Fed Funds Rate. The Prime Loan Rate tends to move along with the Fed Funds Rate and can be calculated by adding 3 points to the Target Fed Funds Rate. If the Fed continues to hike rates, the Prime Loan Rate is likely to increase, which could make borrowing more expensive for consumers and businesses. If the Fed pauses its rate hikes, the Prime Loan Rate may stabilize or even slightly decrease, which could lead to more predictable borrowing costs and potentially stimulate economic activity.

Credit Card Interest

Changes to the Fed Funds Rate can impact credit card interest rates, which are typically expressed as an Annual Percentage Rate (APR). While historically there has been a strong correlation between the Fed Funds Rate and credit card APRs, since 2003 the average APR has been less directly affected by rate changes. Even during the period of low or zero-interest rates, credit card interest rates remained relatively high. Therefore, a pause in rate hikes may not result in a significant change in credit card interest rates. However, it could potentially alleviate some upward pressure on APRs, providing relief to credit card holders and potentially stimulating consumer spending.

Mortgage Rates

Mortgage rates generally track along in the same trend as the Fed Funds rate, experiecing unprecedented lifts during this 2022-2023 hawkish policy. Since February 2022, the 30-Year mortgage rate has climbed 2.5 percentage points to 6.39%. If the current rate hike cycle ends, the 30-Year Mortgage Rate and its 15-Year counterpart might experience a period of stabilization or even a slight decrease, as the 10-Year Treasury Rate could also stabilize or decline. This could lead to more favorable mortgage conditions for homebuyers.

Savings Accounts & CDs

In general, savers or depositors can benefit from Fed rate hikes, as banks raise interest rates on savings accounts and CDs to attract customers. You've likely seen this with local bank advertisements this year.

A pause in rate hikes could lead to a period of stalled interest rates on savings accounts and CDs, as banks job is to create margin between what they loan money out at and how much interest they pay on deposits. This might prompt individuals to seek alternative investment options for better returns, potentially impacting the overall investment landscape, but it would take some time for this discrepancy to unfold.

How Stocks Are Affected by Fed Rate Hikes

Fed rate hikes increase borrowing costs for businesses. This can result in lower top and bottom lines for corporations, leading to reduced stock prices. Growth-focused companies that rely on cheap access to capital may find it more difficult to finance expansion and justify current valuations. This is largely why growth stocks were hammered in 2022.

The stock market has historically thrived in low-rate environments and may still welcome a hike to combat rising inflation. A pause in rate hikes could boost market momentum and offer more attractive financing options, but a restart may make investors less eager to invest in equities.

In Summary

Whatever investments you own or are seeking to acquire, it pays to know the impacts of the Fed Funds Rate so you don’t find yourself “Fighting the Fed”. We hope that the categorical breakdown into topics and how they are affected by the Fed will assist you in your decision making over time.